The Economics and Statistics Division maintains archives of previous publications for accountability purposes, but makes no updates to keep these documents current with the latest data revisions from Statistics Canada. As a result, information in older documents may not be accurate. Please exercise caution when referring to older documents. For the latest information and historical data, please contact the individual listed to the right.

<--- Return to Archive

For additional information relating to this article, please contact:

March 11, 2021EUROPEAN CENTRAL BANK MONETARY POLICY The European Central Bank announced today that key interest rates would remain unchanged at their current levels given the need to continue monetary policy stimulus to support economic recovery and price stability. They are expected to remain at their present or lower levels until the inflation outlook converges to a level sufficiently close to, but below the target rate of 2 per cent consistently.

Euro area real GDP declined 0.7% in Q4, and was down 6.6% overall in 2020. Economic activity was 4.9% below pre-pandemic levels at the end of the year. Weakness is expected to continue in Q1 2021 as the pandemic and containment measures persist. Economic developments will continue to be uneven across countries and sectors with service sectors being more affected by restrictions. Fiscal policy are supporting households and firms, but consumers remain cautious in light of pandemic, employment and earnings. Weaker corporate balance sheet and uncertainty are weighing on business investment.

A firm rebound in economic activity is the current expectation for 2021 as vaccinations ramp-up and containment measures are gradually relaxed. The March 2021 ECB staff projections are broadly unchanged compared to December and are for real GDP to grow 4.0% in 2022, 4.1% in 2022 and 2.1% in 2023.

Risks to euro area growth have become more balanced with better global demand prospects supported by fiscal stimulus and vaccination rollout. Downside risks continue to be related to pandemic and virus variants spreading.

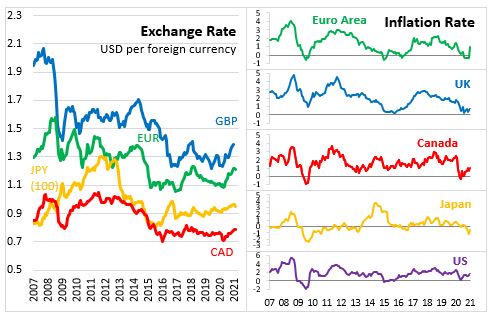

Euro area inflation moved sharply higher to 0.9% in January and February 2021 compared to -0.3% in December 2020. The rising inflation reflects some idiosyncratic factors: ending of temporary VAT rate reduction in Germany, stronger than usual changes in HICP weights, and higher energy prices. Based on rising energy prices, headline inflation is likely to continue to increase in coming months and some volatility is expected throughout the year. Underlying price pressures are expected to rise in 2021 from the current supply constraints and a recovery in domestic demand; however, low wage pressures and past appreciation of euro are expected to keep this pressure subdued overall. Post-pandemic, the unwinding of elevated slack and supportive fiscal and monetary policies will contribute to gradual increase in inflation over medium term. Market-based indicators of long-term inflation expectations remain at subdued levels but continue a gradual rise.

The ECB staff projections are for annual inflation of 1.5% in 2021, 1.2% in 2022, and 1.4% in 2023.

Against this background, the Governing Council reconfirmed its accommodative policy stance. The measures in place include:

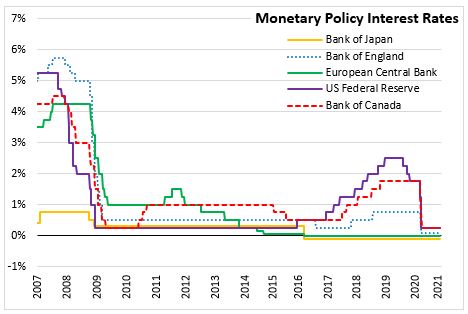

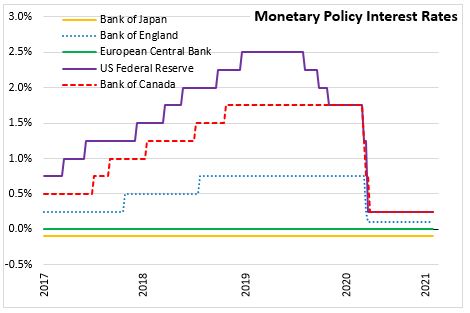

- Interest rate on the main refinancing operations and the interest rates on the marginal lending facility and the deposit facility remain unchanged at 0.00%, 0.25% and -0.50% respectively

- Continuation of net asset purchases under the pandemic emergency purchase programme (PEPP) with a total envelope of €1,850 billion until at least the end of March 2022. The net purchases will continue until the COVID-19 crisis is over.

- Continuation of the reinvestment of principal payments from maturing securities purchased under the PEPP until at least the end of 2023.

- Continuation of net purchases under asset purchase programme (APP) at a monthly pace of €20 billion. Monthly net asset purchases are expected to run for as long as necessary to reinforce the accommodative impact of the policy rates, and shortly before any increase in the key ECB interest rates.

- Continuation of the third series of targeted longer-term refinancing operations (TLTRO III). These conditions will be offered only to banks that achieve a new lending performance target in order to sustain the current level of bank lending.

Source: European Central Bank: Monetary Policy Decision, Remarks

<--- Return to Archive