The Economics and Statistics Division maintains archives of previous publications for accountability purposes, but makes no updates to keep these documents current with the latest data revisions from Statistics Canada. As a result, information in older documents may not be accurate. Please exercise caution when referring to older documents. For the latest information and historical data, please contact the individual listed to the right.

<--- Return to Archive

For additional information relating to this article, please contact:

April 12, 2017BANK OF CANADA MONETARY POLICY The Bank of Canada maintained its target for the overnight rate at 0.5 percent with the Bank Rate continuing at 0.75 per cent and the deposit rate at 0.25 per cent.

Global Growth

Recent data points to a stronger pickup in the global economy, but it must be weighed against considerable uncertainty around US economic policy. Total inflation has recently increased in advanced economies reflecting a recovery in energy prices while core inflation is expected to rise gradually over time.

Global financial conditions continue to be supportive with long-term sovereign bond yields historically low, increases in equity prices and low market volatility measures. Prospects for the euro area have improved but remain modest. Highly accommodative monetary policy, an improving labour market, and increased lending support the economy. Japan's domestic demand has been sluggish with tepid wage growth but a weaker yen and demand from Asia have supported exports. The Chinese economy is performing more strongly than expected amid its rebalancing towards consumption based growth and capital outflows have moderated reflecting tighter capital controls.

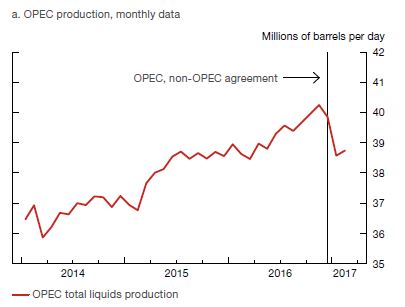

Oil prices have been relatively stable in 2017 even with stronger demand. Reports are that OPEC is having a high degree of compliance with their agreed to production cuts and US crude oil inventories and rigs have increased. Lumber prices have risen with US housing demand and a slowdown in shipments for fear that softwood lumber duties could be applied retroactively. Base metal prices are somewhat higher with past production cuts and global supply disruptions.

US Growth Outlook

The US economy continues to have strong domestic fundamentals to support growth. Consumption growth is supported by anticipated tax cuts and a strong labour market while residential demand will be driven by rising income and demographics. Business investment is expected to turn positive in 2017 with a rebound in the energy sector and strong domestic demand. Net trade will be a drag on growth due to the past appreciation of the US dollar.

The Bank of Canada has moved to incorporated US fiscal stimulus later into the projection horizon reflecting expectation that there will be possible legislative challenges and it will take longer to implement. With the US labour market nearing full employment and core inflation rising, the Federal Reserve raised interest rates in March with further increases expected.

Canada Growth Outlook

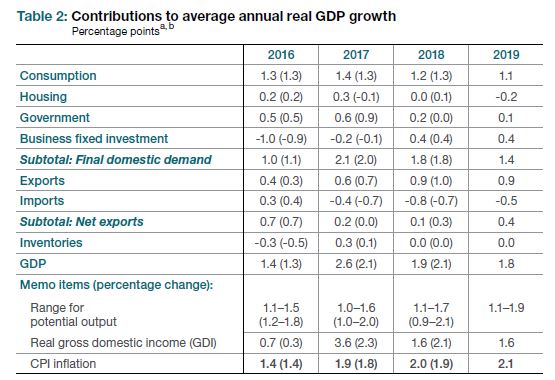

The Bank of Canada expects Canada's GDP to grow by 2.6 per cent in 2017 (up from 2.1 per cent in January), 1.9 per cent in 2018 (down from 2.1 per cent in January) and 1.8 per cent in 2019. Revisions to the outlook for potential output growth has the Canadian economy closing the output gap sooner then previously projected, within the first half of 2018.

Economic growth in recent quarters has been stronger than expected with temporary strength in oil and gas investment, consumption and residential investment. However, non-commodity business investment and exports remain weak, suggesting that the pace will not be sustained in the medium term.

The Canadian economy is expected to grow at moderate pace supported by rising foreign demand, federal fiscal stimulus and accommodative monetary and financial conditions. Residential and to a lesser extent household expenditures are expected to moderate with greater contributions coming from exports and investment. However, ongoing competitiveness challenges and uncertainty around trade protectionism will limit expansion.

Inflation Outlook

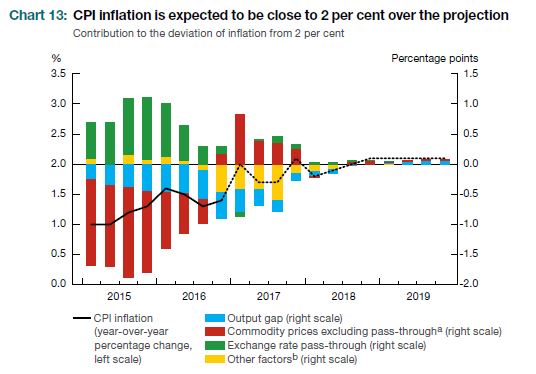

CPI inflation is expected to ease to 1.7 per cent by the middle of 2017 as upward pressure from consumer energy prices dissipates. Weaker food prices, electricity rebates and excess supply weigh on inflation. Projected inflation over second half of 2017 will be around 2 per cent as factors dissipate before returning sustainable to the 2 per cent target in the first half of 2018.

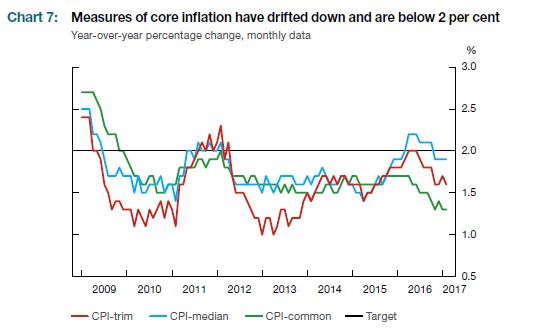

The Bank now uses three new measures of core inflation to obtain a more reliable gauge of the underlying trend of inflation. These measures have declined since mid-2016 to below 2 per cent, and are broadly consistent with the Bank’s assessment of the degree of excess capacity in the Canadian economy.

The next scheduled date for announcing the overnight rate target is 24 May 2017. The next full update of the Bank’s outlook for the economy and inflation, including risks to the projection, will be published in the MPR on 12 July 2017.

Bank of Canada Press Release, Monetary Policy Report.

<--- Return to Archive